Net worth is a concept used by businesses and individuals to assess their financial position. It is used in terms of checking how rich or poor people are, and in this post, we will be discussing the basics behind it and how you can calculate your own net worth.

Have you ever calculated your net worth? It’s simple to do with most personal finance software. Calculating your net worth is a great way of knowing where you currently stand financially, to check where you want to be, and what progress you are making towards that goal.

Net worth is a figure that represents the total assets of a person. In short, net worth is calculated as assets – liabilities. Your net worth is basically the value of all your assets minus your liabilities. This article will outline how to calculate your net worth.

Determining Assets

When you calculate your net worth, you first need to decide what assets you have. Let’s look first at assets that you can touch and hold in your hands. First are the things you own or have access to. This includes your home or car; the household items or clothes you own; your tools and computer; the books you own; the money you or someone else has given you; the investments you own; and so on.

Next are the things you own with a title, like a stock or bond. Ownership of these things may be debt or equity, and they may be held in your name or someone else’s. Finally, there are the things you own but don’t have title to, like a bank account or a life insurance policy.

The amount you are worth is the difference between your assets and your liabilities. There are two ways of looking at this. One is from the point of view of how much you owe, and the other is how much you own.

The debt-to-asset ratio tells you how much you owe. If you have a mortgage of $100,000, and your home is valued at $150,000, then you have a debt-to-asset ratio of $50,000. The equity-to-asset ratio tells you how much you own. If you have a home worth $150,000, and if you sell it for $200,000, you have a 50 percent equity-to-asset ratio of $100,000. The net worth-to-asset ratio tells you how much you own relative to your debts. If you have a net worth of $100,000, and if you owe $50,000, you have a 50 percent net worth-to-asset ratio.

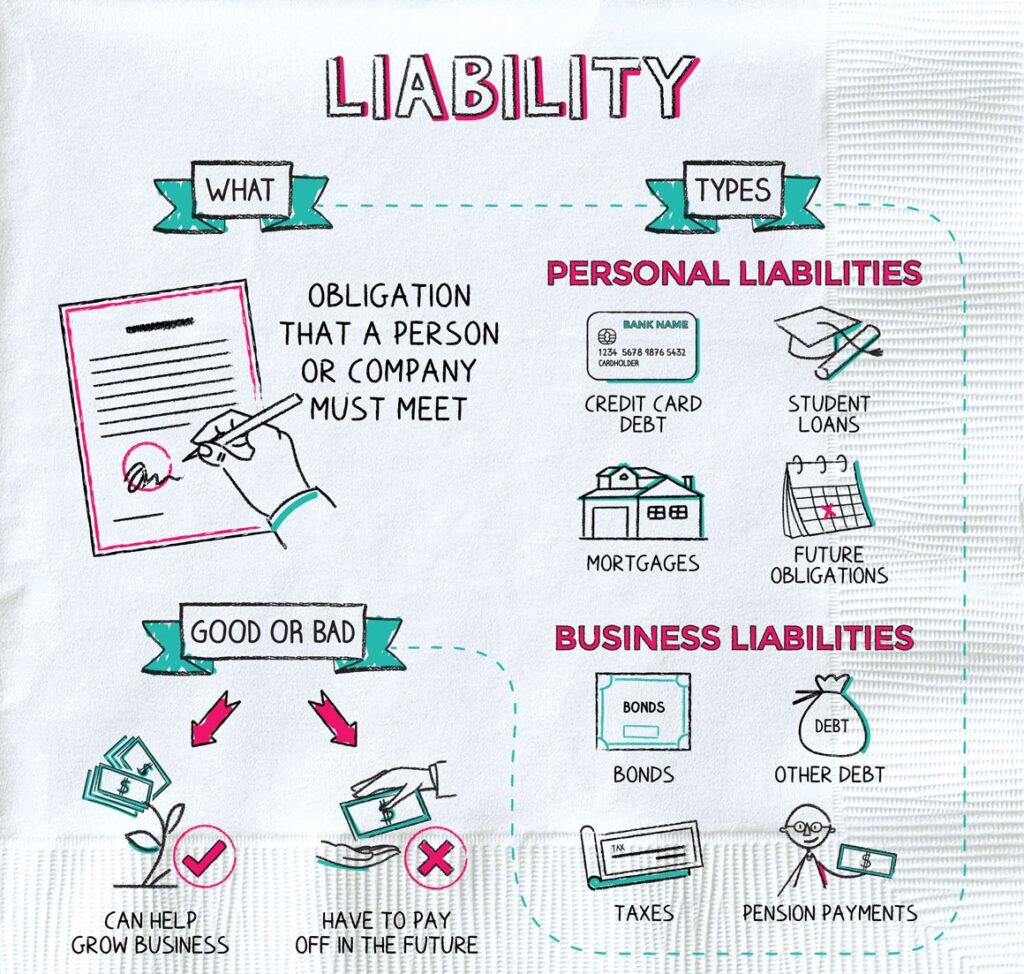

Determining Liabilities

A liability is an obligation. That means that your liabilities are obligations you owe. To start, take out any debts you might have — like a mortgage on your home — and write them down.

Then add up all your assets. Your home and your car, for example, are assets. Your savings account and your stocks are assets. Now add up all your liabilities. Your student loans and your car loans are liabilities. Your credit card debt is a liability.

Simple Formula to Calculate Net Worth

Your net worth is determined by three things:

1. Your assets

2. Your liabilities

3. The percentage that your assets make up of your net worth. Now, calculate your net worth again, but look only at your liabilities. If you have $50,000 in assets and $25,000 in liabilities, you have a net worth of $25,000our net worth will change every day.

When you make an investment, you increase the value of some of your assets, and you decrease the value of some of your liabilities. That change, plus any change that happens because of market changes, will decrease your net worth. You can see your net worth change whenever you want by using online banking. For example, if you log in to your bank online or through their smartphone app and you can check your investment account, your savings, your credit cards, your checking account, and your assets and liabilities, You can use the same app to see how much money you earned and how much you spent.

If you really want to know the value of your assets, you can use a service like Bankrate.com, which allows you to track the value of your investments and the value of your home. It can also help you calculate how much money you’ll make in interest and how much money you’ll save by paying off your loans early.

It’s a good idea to keep track of your net worth every month. That way you can see how your decisions affect your wealth. It’s a good idea to keep track of your net worth every month. That way you can see how your decisions affect your wealth

Advantages of Tracking Net Worth

A lot of us have heard about the concept of net worth but don’t really understand what it really means or why we would want to track it.

Why track net worth?

When we track our net worth, we are essentially tracking our financial health. Doing so allows us to gauge how much progress we have made in paying off our debts or saving for the future. Also, when we track our net worth, we essentially are creating our own personal budget.

Our net worth is fluid. It fluctuates depending on our expenses, income, and savings. For example, we may spend some money on a car, and this may cause our net worth to decrease. However, when we sell the car, our net worth increases. Tracking net worth is important because it helps us keep a perspective on our financial health. It helps us allocate our money more effectively.

How to track net worth?

There are several different ways that you can track net worth. You can track it manually, by using a net worth calculator, or by using the software.

Manually Tracking net worth manually can be a bit tedious, but it can be done. For example, you can track your net worth by writing it down in a journal or spreadsheet.

Net Worth Calculator: A net worth calculator is a handy tool, especially if you tend to forget the numbers. There are a wide variety of software programs available to help you track net worth. Some popular options include Personal Capital, Quicken, etc

Calculating your net worth isn’t complicated, but it does require some financial information, so it’s important to be organized and to periodically update the information.

To calculate your net worth, you’ll need (but are not limited to):

• Your current bank balance

• Your retirement accounts

• Your checking and savings accounts

• Your mortgage

• Your car payments

• Your student loan payments

• Your credit card debt

• Receipts or credit card statements

• Your property tax bill

• Your student financial aid

• Your health insurance

• Your life insurance

• Your disability insurance

• Your emergency fund

• Your investment accounts

Conclusion: Now that you have learned about the basics of Net Worth, Assets and Liabilities it is advisable to start your calculation now. The best way to become wealthy is to start now. The longer you wait, the bigger the habit you need to break.